Biomethane in Malaysia: Turning waste into a strategic energy source

As Malaysia looks to decarbonise its energy systems, biomethane is increasingly viewed as a viable alternative to natural gas. Produced from organic waste, it has strong potential to support the nation’s energy transition, circular economy and net zero ambitions. Could biomethane become one of Malaysia’s strategic energy source in the future?

What is Biomethane?

Biomethane, also known as renewable natural gas (RNG), is a near-pure source of methane produced either via biogas upgrading or biomass gasification followed by methanation. According to IEA, about 90 percent of global biomethane supply is derived from biogas upgrading.

Biogas (precursor to biomethane) is produced through anaerobic digestion (AD), a biological process in which microorganisms decompose organic wastes (i.e., agricultural residue, animal manure, organic portion of landfill waste) in the absence of oxygen. If left unmanaged, the waste streams would release methane - a greenhouse gas 28 times more potent than carbon dioxide (CO2) - into the atmosphere. Valorising these waste streams not only reduces GHG emissions but also creates a clean energy source in the form of biomethane.

Biogas produced through AD typically contains 45 to 75 percent methane, along with CO2 and trace contaminants. The raw biogas subsequently undergoes an upgrading process, where CO2 and trace contaminants are removed, resulting in a biomethane stream that contains at least 95 percent methane. Biomethane is indistinguishable from natural gas, allowing its direct use across power, industrial, and transport applications. To facilitate storage and transportation, biomethane is converted into bio-compressed natural gas (bio-CNG) or bio-liquefied natural gas (bio-LNG).

Figure 1 Malaysia Biomethane Process Overview

Overview of Malaysia’s Biomethane Market

While biomethane can be produced from a range of organic feedstocks, Malaysia’s production predominantly uses palm oil mill effluent (POME). As the world’s second largest palm oil producer, the country is estimated to generate around 50-75 million m3 of POME annually, making it the most abundant and viable feedstock for biomethane production.

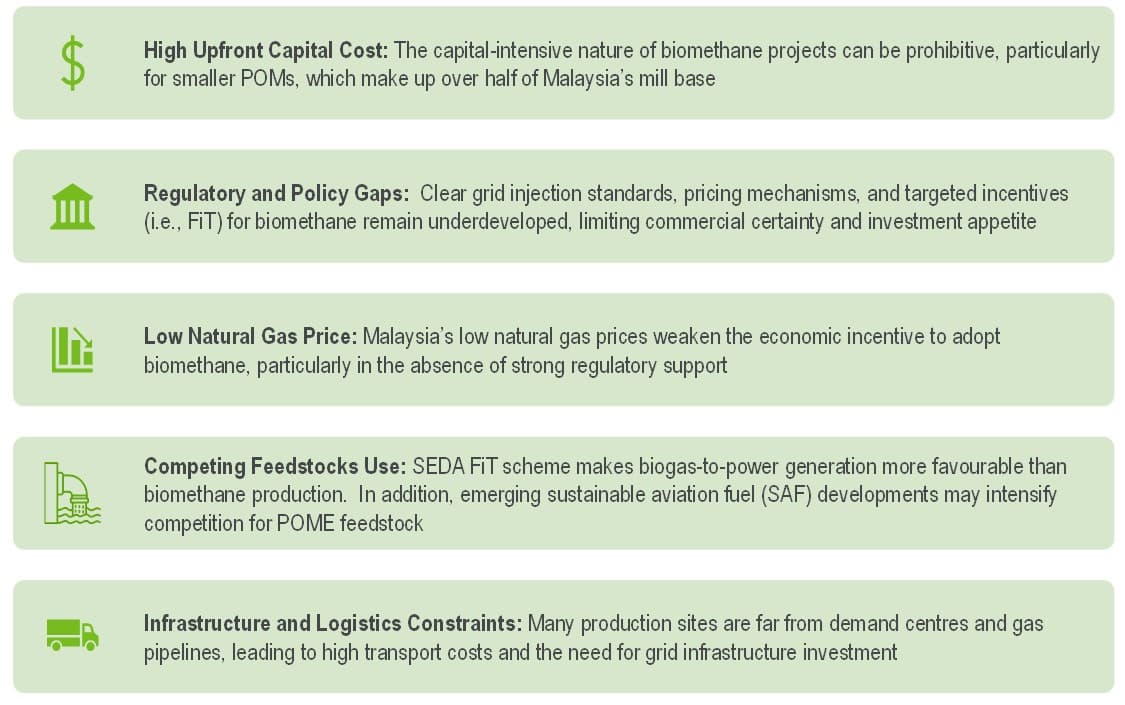

Malaysia has around 450 palm oil mills (POMs), but only one third of them are equipped with methane capture facilities. Majority of the POMs with methane capture facilities utilise biogas directly for captive power generation, with surplus power exported to the main grid under the existing Feed-in Tariff (FiT) mechanism administered by the Sustainable Energy Development Authority (SEDA). Currently, there are only four sites in the country with the capability to upgrade biogas into biomethane. As additional CAPEX is required to install biogas upgrading facilities, these biomethane plants are typically associated with larger POMs that allow producers to benefit from economies of scale.

Malaysia’s first biomethane plant, located at Sungai Tengi, Perak, is also the world’s first biomethane facility based on POME. The plant commenced operations in 2015 and has an estimated biomethane capacity of two thousand tons per year. Since then, three additional POME-based biomethane plants have come online in Malaysia. These plants are located at the Coronation and Sedenak mills in Johor, and the Apas Balung mill in Sabah. This brings the total biomethane capacity in the country to around 10-15 thousand tons per year in 2025.

While biomethane can also be produced from landfill gas, existing landfill-based biogas facilities in the country today are mainly configured for power generation.

Existing energy policy frameworks in Malaysia are predominantly concentrated on the utilisation of biogas for electricity generation. For example, under the Malaysia Renewable Energy Roadmap (MYRER), the government aims to achieve 40 percent renewable energy share in the electricity sector, with around 400 MW coming from biogas. Malaysia’s National Energy Transition Roadmap (NETR) also outlines targets to increase biomass and biogas power generation capacity to 1.4 GW by 2050. These frameworks do not include specific targets or plans for biomethane or bio-CNG production. Other key challenges limiting the adoption of biomethane in Malaysia include the following:

Key Challenges for Biomethane Adoption in Malaysia

Key Drivers and Opportunities for Biomethane

Malaysia’s biomethane market is likely to remain supply-driven due to the lack of regulatory policies targeting biomethane consumption. The country’s low natural gas price also provides little incentive for existing consumers to switch to biomethane. Majority of existing biomethane production today is injected into the main gas grid and supplied to the industrial sector, with some volumes distributed to nearby manufacturing facilities via compressed natural gas (CNG) trucks.

Near term biomethane adoption is driven primarily by voluntary efforts to reduce carbon emissions in the industrial and manufacturing sectors. For example, Gas Malaysia, the main gas supplier in Malaysia, is committed to achieving net zero emissions by 2050, focusing on integrating renewable gases including biomethane in their gas distribution networks. In 2025, the company established Malaysia’s first centralized biomethane injection station in Johor. Gas Malaysia also collaborated with industrial customers such as Intercontinental Specialty Fats (ISF) on the supply of ISCC-certified biomethane.

Malaysia’s biomethane supply is projected grow robustly at around 30 percent CAGR through 2030, driven by announced biomethane projects and efforts to establish centralised injection points at the main gas grid in Peninsular Malaysia. Several POME-based projects such as the Pintasan, Tereh and Sindorah plants are expected to come online in 2026. In addition, two upcoming landfill gas-based projects at Teluk Mengkudu and Ampang Jajar signal early diversification beyond POME feedstocks, with commissioning expected in the next two to three years. Majority of these projects are in Peninsular Malaysia, with proximity to Gas Malaysia’s main gas transmission line along the west coast.

In the longer term, biomethane consumption is expected to increase with anticipated implementation of carbon taxes in Malaysia, driving natural gas consumers to shift towards low carbon fuels. Global regulatory developments such as the International Maritime Organisation’s (IMO) Net Zero Framework and FuelEU Maritime, which outline GHG emissions targets and associated emissions pricing mechanisms for the shipping industry, is also anticipated to drive demand for bio-LNG especially in neighbouring Singapore, a major bunkering hub in Asia.

Authors:

Naveen Markandan, Analyst

Jia Lin Chong, Senior Consultant

About Us - FGE NexantECA is the leading advisor to the energy, refining, and chemical industries. Our clientele ranges from major oil and chemical companies, governments, investors, and financial institutions to regulators, development agencies, and law firms. Using a combination of business and technical expertise, with deep and broad understanding of markets, technologies, and economics, FGE NexantECA provides solutions that our clients have relied upon for over 50 years.

Contact a member of our team to see how we can support your operational, investment, or trading decisions